One of the most imperative questions at the moment, insofar as the Philippines’ economy is concerned, is whether the country has collapsed into the “sick man of Asia” once again, a caricature once attached to the years of President Ferdinand Marcos Sr. But the sharper question is whether it is drifting toward a subtler, equally damaging condition and chronic underperformance masked by short-term buffers.

Let’s Start with the Facts

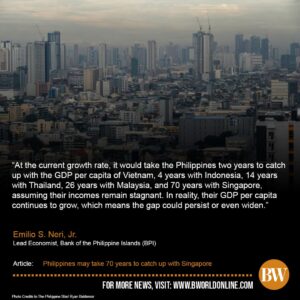

Growth has slowed materially. The full-year GDP growth in 2025 came in at 4.4%, with fourth-quarter growth weakening to 3.0%, the weakest pace in years. This is not catastrophic, but it is insufficient to transform poverty dynamics or accelerate structural upgrading. Momentum matters.

Moreover, investment contraction late in the year is especially concerning because investment, not consumption, is what sustains productivity gains. According to the Philippine Statistics Authority, gross capital formation (investment) contracted by 5.7% in real terms in the fourth quarter. This means that overall investment in the economy, including private and public spending on fixed assets, was not just stagnant but also shrinking late in the year, even as consumption continued to support growth.

This contraction is important because investmentis the driver of future productive capacity- infrastructure, factories, machinery, and technology, whereas consumption mostly supports current output. Falling investment signals weakening confidence and fewer capital projects, which tend to weigh down potential growth over time.

The labor market tells a mixed story. Unemployment averaged roughly 4.2% in 2025, moderate by historical standards but slightly worse than the previous year. Headline figures obscure underemployment and concerns about job quality, particularly in informal and low-productivity sectors. Growth that does not translate into quality employment is growth without lift.

Fiscal conditions are stable but tightening. National government debt reached a record nominal level, around ₱17.7 trillion, with a 63.2% debt-to-GDP ratio in 2025, a 20-year high that exceeded the commonly cited 60% “manageable” threshold. This is not a debt crisis yet; if borrowing is used to build productivity-enhancing infrastructure, energy reliability, logistics efficiency, and human capital. But if it finances leakages, inefficiencies, or politically expedient spending and corruption, it compounds vulnerability.

Whereas gross international reserves remain above $110 billion, providing a buffer against shocks. Remittances, over $35 billion, continue to support domestic consumption and foreign exchange liquidity. Yet the current account remains in deficit, and the peso has weakened. The economy is still structurally reliant on remittance-supported consumption and import-intensive growth. That model cushions shocks, but does not necessarily build competitive depth.

Indeed, under Marcos Jr.’s government, the Philippines is not yet comparable to the “sick man” moment of the Marcos Sr. era. Not yet in the immediate. It is stagnation by erosion. However, if investment continues to slow, massive corruption in government persists, infrastructure integrity falters, industrial competitiveness lags behind regional peers, and fiscal consolidation constrains productive spending, the Philippines risks returning to the 1980s “Sick Man of Asia.”

Source: The Lobbyist

https://www.thelobbyist.biz/perspectives/article-details/prime%20insight/sick-man-of-asia-again-relapse-or-resilience