Slapping the Filipino people, especially low- to middle-income Filipinos, with a 20% tax on savings, as part of Republic Act No. 12214 (also known as the “Ease of Paying Taxes Act”), is another tax measure that squeezes the take-home pay of low-to middle-income Filipinos. Lest we forget, Filipinos are already heavily taxed, yet public service is poor and not satisfactory in comparison to neighboring countries.

Folks, below is a general breakdown of the various taxes imposed on Filipinos, starting with automatic income deductions. This is followed by a critical insight into how these taxes affect disposable income, as well as the implications of the 20% tax on savings, particularly in light of fluctuating inflation.

🇵🇭 A. Automatic Deductions from Salaries (Payroll Taxes). These are the standard deductions every salaried Filipino employee sees on their pay slip.

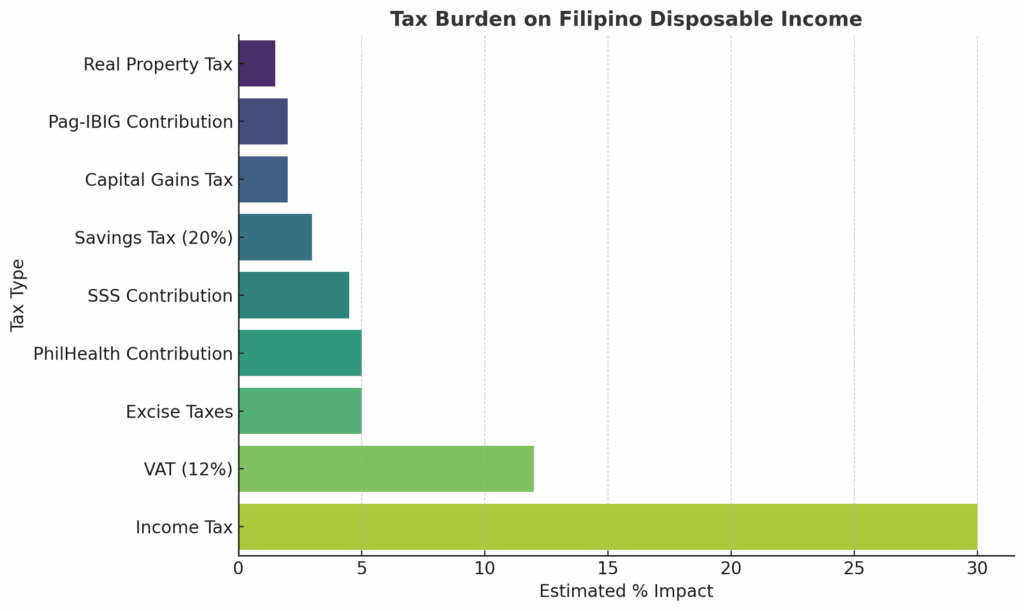

- Income Tax (Withholding Tax). The progressive rates are 0% to 35%, depending on the income bracket. Additionally, you have PhilHealth contributions or other mandatory health insurance, as well as Pag-IBIG Fund contributions. Roughly, the total deductions from gross pay can range from 25% to 35%, depending on income level.

- Consumption-Based Taxes (Indirect Taxes) like the Value-Added Tax (VAT). Approximately 12% on most goods and services, from groceries to utility bills. Paid by everyone, regardless of income level, which is regressive in effect. Then there’s the Excise Taxes applied to “sin products” like alcohol, tobacco, sugary drinks, petroleum, and luxury items.

- Additionally, there are fuel and oil excise taxes, which are a major driver of inflation, affecting transportation and food prices.

- Likewise, there are taxes on wealth, property, and business. Real Property Tax (RPT) is paid annually by landowners to LGUs, which is based on the property’s fair market value. Estate and Donor’s Tax, approximately 6% flat rate after applicable deductions. Capital Gains Tax, approximately 6% on the sale of real property, approximately 15% on the sale of stocks not traded on the stock exchange. Business and Self-Employed Taxes, which apply to Freelancers, SMEs (Small and Medium Enterprises), and professionals, are paid as a percentage tax or income tax, depending on gross receipts.

- And here comes the New and Special Taxes. 20% Withholding Tax on Savings Interest (RA 12214) is being positioned by Finance Secretary Ralph Recto as a measure to boost government revenues and streamline the tax system. This policy raises several critical concerns, especially for ordinary Filipinos.

Is the Marcos Jr. government truly incapable of imagining any other revenue-generating strategy besides squeezing already overtaxed Filipinos dry or going on a borrowing binge from every available lender, be it the ADB, World Bank, IMF, or the neighborhood pawnshop? With the national debt already soaring past ₱17 trillion, you’d think someone in power might consider stimulating actual economic productivity instead of defaulting to the same old formula: tax, borrow, repeat. But no! Why innovate when you can just mortgage the country’s future one loan at a time? Bravo!

Folks, while the government of Marcos Jr. claims that a 20% tax on savings (passive income), particularly on interest, not the principal, will help reduce the deficit, it’s the ordinary Filipino, low-income savers, retirees, and minimum wage earners who bear the brunt. Here’s the thing, folks,

📉 Small Interest, Big Tax! This will disincentivize saving in banks, especially at a time when interest rates on deposits are already low, ranging approximately or more or less from 1.5 to 2% annually. For instance, a minimum-wage earner who saves ₱100,000 in a bank account earning 1.5% interest annually would get ₱1,500. After deducting the 20% withholding tax, they receive only ₱1,200, barely enough to keep pace with inflation. Hence, this will encourage people to keep money in cash or informal instruments, weakening financial inclusion and the banking system. More importantly, this is an epitome of worsening wealth inequality in the country, as it taxes small savers, while capital gains on stocks and other high-end investments remain more favorable and accessible only to the wealthy, who comprise around 1% to 2% of the population.

📊 ₱25B Gain vs. Financial Exclusion Risk?: The Bangko Sentral ng Pilipinas (BSP) promotes banking, encourages financial literacy, and fosters financial inclusion. Then why push people to save in formal institutions, then penalize them for doing so? Small savers, especially those in rural areas or the informal sector, are discouraged from joining the formal financial ecosystem due to such a policy, which sends the wrong message: saving is no longer rewarded—it’s now taxed.

Moreover, the revenue justification is a weak argument and short-term. Recto projects only ₱25 billion in revenue through 2030, or about ₱3.5 billion annually. This is minimal compared to the total budget deficit of around ₱1.5 trillion in 2024. The harm it causes to savings behavior and financial trust may far outweigh the modest gains. If the goal is fiscal consolidation, progressive wealth taxes, digital economy taxation, or stricter enforcement of tax evasion would be more equitable and efficient.

🤔 Is it Really Tax Reform, or Just Another Regressive Policy disguised as progress?: This policy has a regressive impact compared to wealthier Filipinos. Note that the tax is flat and applies uniformly regardless of the amount of savings. This makes it regressive; it takes a higher relative toll on those with less money. High-net-worth individuals have access to tax-free or tax-advantaged investments (e.g., government bonds, equities, REITs, offshore funds). Meanwhile, ordinary Filipinos rely on savings accounts and time deposits, which are now taxed at the same rate as someone earning millions in passive income. This ultimately burdens the bottom majority more than the top percentile.

Lest we forget, this tax is being implemented at a time of fluctuating inflation, stagnant wages, and economic uncertainty. Filipinos are already struggling with the pressures of a high cost of living. Raising the effective tax burden, even on passive income, adds insult to injury. It’s politically tone-deaf: the perception is that ordinary Filipinos are made to pay more, while the rich, corrupt, or powerful are off the hook.

📉 Impact on Disposable Income Amid Fluctuating Inflation: Indeed, given all these, the wallets of Filipinos are being squeezed tightly. The financial burden on ordinary Filipinos has reached a breaking point. Even before workers can spend their earnings, hefty income deductions significantly reduce their take-home pay. What’s left is then relentlessly eroded by inflation, especially in essential sectors such as food, fuel, and transportation, while consumption taxes like VAT and excise taxes continue to rise proportionately with prices.

This double whammy, diminishing real wages and increasing cost of living, is further aggravated by a tax system that, while progressive on paper, is regressive in practice. Flat-rate consumption taxes disproportionately hit the poor, who spend most of their income on basic goods and services.

These recent measures, such as the 20% tax on savings interest, add insult to injury, punishing even the modest attempts of Filipinos to build a financial cushion. And behind every purchase, whether utility bills, toll fees, prepaid load, or a simple fast-food meal, lurks an embedded tax that silently chips away at what little remains of disposable income.

The result? A shrinking middle class, growing financial insecurity, and fewer opportunities for upward mobility. What’s unfolding is not just an economic crunch, but a silent crisis of equity and survival.

Food for Thought:

Mr. President Marcos Jr. maybe what you should do if quite have the time away from photo ops, etc. is look at how you can possibly reform further the tax system of the country that includes adjusting tax brackets to account for inflation, lowering the VAT on essential goods, exempting small savers, and shifting the tax burden toward high-net-worth individuals or the wealthy in the country not penalize the lower-to-middle income Filipinos.

Why? Currently, the message is clear: in the Philippines, earning is taxed, spending is taxed, and even saving is taxed, leaving the average Filipino trapped in a cycle of economic and tax exhaustion. Goodness gracious!

Mr. President, suppose your government claims to be serious about closing the fiscal gap. In that case, it should target wealth more than savings, evasion more than inclusion, and privileged sectors more than struggling savers —the low- to middle-income Filipinos.

Mr. President Marcos Jr.’s savings should be rewarded, NOT penalized. You should rethink this!

#TaxReform

#RA12214

#SavingsTax

#EconomicJustice

#FinancialInclusion